Industry is central to economic development, yet it is also one of the most significant contributors to climate change. Manufacturing and industrial processes account for roughly 40 % of global carbon dioxide emissions (around 16 GtCO₂ per year), with heavy sectors such as steel, cement, and chemicals particularly emissions‑intensive (OECD, 2021). Emerging economies — including India, Indonesia, South Africa, Brazil, and Mexico — face the dual challenge of sustaining industrial growth while meeting commitments under the Paris Agreement and national net-zero ambitions.

Despite increasingly ambitious climate pledges, translating high-level targets into concrete policy frameworks and investment-ready programmes remains difficult. Many countries lack sector-specific strategies, coherent incentive structures, robust financing mechanisms, and comprehensive measurement, reporting, and verification (MRV) systems. These gaps not only slow project implementation but also limit private investment and risk locking in high-carbon industrial pathways.

Industrial decarbonisation in emerging economies is further complicated by technological lock-ins, energy access constraints, and governance fragmentation, where growth and climate priorities are often misaligned. Yet, opportunities exist: energy efficiency improvements, low-carbon material innovation, and green manufacturing can reduce operational costs, create jobs, and improve local air quality.

Addressing these challenges requires domestic policy reform supported by sustained international cooperation. Multilateral organisations, technical partnerships, climate finance mechanisms, and regional development banks play a pivotal role in bridging ambition and action, helping to transform industrial decarbonisation from aspiration into measurable, scalable outcomes.

Heavy industry remains a cornerstone of economic development in emerging economies, providing essential materials, capital goods, and employment for infrastructure, construction, and national productivity. Yet these same sectors are responsible for a disproportionately large share of greenhouse gas emissions. For example, in Turkey, the industrial sector contributed roughly 75 MtCO₂ — around 13 % of national emissions — in 2021, with iron and steel production among the largest sources (Wikipedia, 2025). Similarly, in India, industrial emissions have grown rapidly alongside GDP, with cement and steel production among the fastest-growing sub-sectors.

Heavy industry—including manufacturing, construction, and industrial process emissions—accounts for a significant share of national emissions. The chart below, reproduced from Our World in Data, illustrates greenhouse gas emissions by sector and country, highlighting the considerable share of emissions contributed by heavy industry.

“Maintaining industrial growth while limiting emissions is not simply a technical problem, but a structural one.”

This dual role creates a fundamental trade-off: maintaining industrial growth while limiting emissions is not simply a technical problem, but a structural one. Many industrial facilities in emerging economies rely on energy- and carbon-intensive processes that have long lifespans, creating technological “lock-ins” that slow the adoption of low-carbon alternatives. Retrofitting older blast furnaces, cement kilns, or chemical plants often requires multi-million or even multi-billion-dollar investments — a prohibitive cost for both private enterprises and public budgets without access to concessional finance or policy incentives.

“Industrial facilities in emerging economies rely on energy- and carbon-intensive processes that have long lifespans, creating technological ‘lock-ins’ that slow the adoption of low-carbon alternatives.”

Energy access and affordability further complicate the trade-off. Electrification of industrial heat, green hydrogen, or carbon capture and storage (CCUS) technologies require reliable, competitively priced energy, yet grids in many emerging economies are constrained, and renewable energy integration remains uneven. High electricity tariffs or intermittent supply can render low-carbon solutions economically unviable compared with fossil fuel options, slowing the pace of decarbonisation.

Industrial emissions are also deeply interconnected with other sectors. Cement and steel used in urban infrastructure, for example, generate indirect emissions through construction and transport, demonstrating the “embedded carbon” effect. Effective decarbonisation therefore requires holistic strategies that account for upstream and downstream linkages, rather than treating industrial sectors in isolation.

Policy and governance challenges add another layer of complexity. Even where ambitious net-zero targets exist, fragmented institutional mandates, limited technical capacity, and regulatory uncertainty often impede implementation.

Industrial policy tends to prioritise growth and competitiveness, while climate policy focuses on emissions reduction; misalignment between these priorities can slow the translation of national targets into sector-specific action.

Despite these challenges, industrial decarbonisation offers significant co-benefits that can help reconcile growth and climate objectives. Improvements in energy efficiency, low-carbon material innovation, and green manufacturingcan reduce operational costs, create new jobs, and improve local air quality. Highlighting these co-benefits strengthens the case for ambitious yet feasible policies, showing that climate action can complement, rather than compromise, economic development.

This complex dynamic between industrial growth, emissions intensity, and policy capacity underscores why sector-specific strategies and targeted support are essential. Without such interventions, emerging economies risk locking in high-carbon pathways even as they pursue development, highlighting the urgency for comprehensive policy design and implementation frameworks.

While the dynamic between industrial growth and emissions intensity underscores the urgency of decarbonisation, translating this urgency into actionable strategies reveals persistent policy gaps that hinder effective implementation in emerging economies.

A significant barrier in emerging economies is the lack of recognition of industrial decarbonisation as a coherent policy domain. While governments may pursue energy efficiency, emissions reduction, and industrial growth, these efforts are often fragmented across different ministries and programmes. Without identifying industrial decarbonisation as a distinct sectoral priority, initiatives remain siloed, incentives misaligned, and investment pipelines underdeveloped.

“Without identifying industrial decarbonisation as a distinct sectoral priority, initiatives remain siloed, incentives misaligned, and investment pipelines underdeveloped.”

Recognising it as a cohesive policy area allows for coordinated strategies, clearer intermediate targets, and integrated technical, financial, and regulatory interventions — creating a foundation for translating ambition into tangible implementation.

Many national climate plans in emerging economies articulate high‑level decarbonisation goals, yet lack sector‑specific pathways or intermediate milestones tailored to heavy industry. Without such detailed strategies, policymakers and investors are left without clear signals on technology adoption timelines, regulatory expectations, or compliance frameworks.

Economic incentives are crucial for shifting industry investment toward low‑carbon technologies. However, global adoption of carbon pricing instruments remains limited: only around 23 % of greenhouse gas emissions are currently covered by meaningful carbon pricing regimes, with prices often set below levels needed to drive substantial behavioural change in industry (World Bank, 2023).

In many emerging economies, fossil fuel subsidies persist, reinforcing the economic attractiveness of high‑carbon processes and weakening the competitiveness of clean alternatives. The absence of robust carbon markets, tax incentives or tradable performance standards therefore limits the policy toolkit available to industrial decarbonisation.

Industrial decarbonisation is capital‑intensive, particularly where new processes involve advanced technologies such as carbon capture, utilisation and storage (CCUS), electrolysis‑based green hydrogen, or fuel switching.

Research shows that of 826 proposed clean industrial projects across 69 emerging and developing economies, only 69 were operational and 65 had received secured financing, meaning over 80 % of the potential pipeline remains unfinanced (FT, 2025). In India, for instance, while 53 clean industrial initiatives were under consideration in a recent year, only two projects reached a final investment decision, largely due to financing, regulatory uncertainty and infrastructure constraints (Reuters, 2025)

Public and concessional climate finance programmes, such as the Climate Investment Funds’ Industry Decarbonization Investment Programme, are beginning to address these gaps by mobilising blended finance aimed at attracting multiple times in co‑investment from development banks and private capital (Reuters, 2025).

The effectiveness of industrial decarbonisation policies ultimately depends on private sector participation. Firms are the primary actors implementing energy efficiency measures, adopting low-carbon technologies, and restructuring production processes. Policy gaps — such as weak incentives, unclear regulations, or financing constraints — can disincentivize private investment, delaying deployment of low-carbon solutions. Conversely, well-designed policy frameworks, clear sectoral roadmaps, and targeted financial support can mobilise private actors to scale innovation and operational changes.

Emerging economies face additional challenges, as industrial sectors often include a mix of state-owned, small, and informal enterprises with differing capacities to respond to policy signals. Recognising this heterogeneity is essential: not all firms react equally to incentives, carbon pricing, or regulatory mandates. Policies must therefore be tailored to actor type, combining technical support, financial mechanisms, and regulatory clarity to unlock private investment in decarbonisation.

“Not all firms react equally to incentives, carbon pricing, or regulatory mandates. Policies must therefore be tailored to actor type.”

By highlighting the diversity of industrial actors and the tailored policy levers required, this approach reinforces the central role of the private sector in translating net-zero ambitions into practical, scalable outcomes. Combined with public policy, international support, and financial mechanisms, engaging these actors strategically is critical to closing implementation gaps in emerging economies.

Accurate emissions data is foundational for credible policy, carbon pricing, investor confidence and regulatory enforcement. Yet many emerging economies lack comprehensive MRV systems, resulting in incomplete or inconsistent emissions inventories (WRI, 2023). This undermines government capacity to target high‑intensity processes, evaluate policy effectiveness, or link emissions performance to financial incentives.

Emerging economies face unique structural and economic factors that intensify these policy gaps. Rapid industrialisation reliance on energy-intensive sectors, and constrained fiscal space limit governments’ ability to implement large-scale decarbonisation measures. Many industries are dominated by older, carbon-intensive infrastructure with long payback periods, making technology transitions costly and politically sensitive. Additionally, competing development priorities—such as job creation, energy access, and infrastructure expansion—can conflict with aggressive emissions reduction targets.

Limited domestic technical expertise and fragmented governance structures further impede the coordination of sector-specific strategies, financing mechanisms, and MRV systems. Taken together, these factors mean that emerging economies are often balancing the dual imperatives of economic growth and climate action, creating a particularly challenging environment for translating net-zero ambitions into practical industrial decarbonisation outcomes.

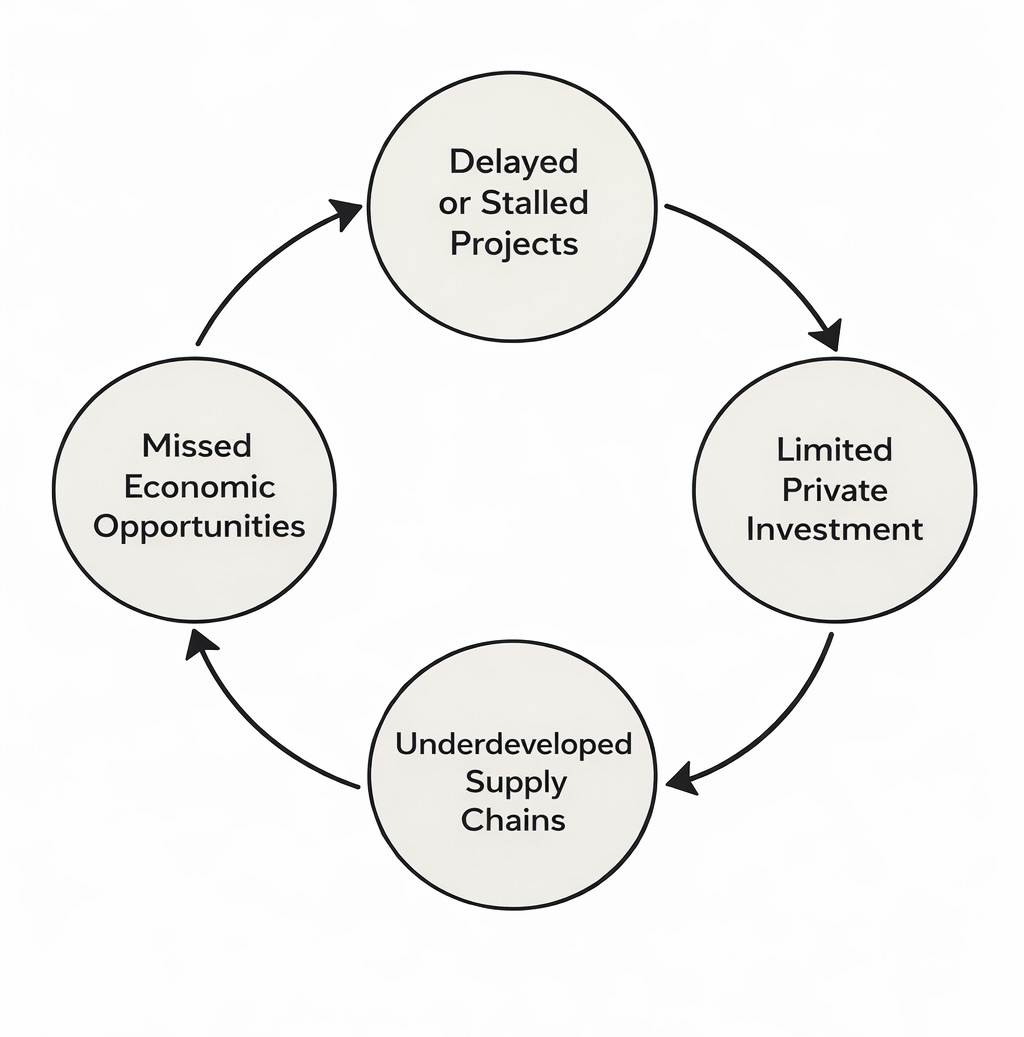

Policy gaps have direct and multifaceted consequences for the pace and scale of industrial decarbonisation.

- Delayed or stalled projects: Without clear sector-specific pathways and regulatory certainty, investors are likely to postpone capital commitments, particularly for technologies with long payback periods, such as carbon capture, green hydrogen, or low-carbon cement production.

- Limited private investment: Weak incentives, inconsistent enforcement, and uncertain revenue streams reduce the appeal of industrial decarbonisation projects to commercial financiers. This limits the mobilisation of private capital, which is essential given the capital-intensive nature of industrial transitions.

- Underdeveloped supply chains: In the absence of coordinated policy signals, domestic industrial ecosystems struggle to develop markets for low-carbon inputs, including green steel, alternative cements, and energy-efficient machinery. This hinders the ability of emerging economies to build competitive, decarbonised industrial sectors.

- Missed economic opportunities: Econometric analyses indicate that targeted industrial decarbonisation in regions such as East Asia could unlock up to USD 1.7 trillion in investment opportunities and abate the equivalent of 16 % of global carbon emissions by 2050 — yet these gains depend on strategic policy, financing, and coordination (Forbes, 2025).

Beyond these immediate effects, policy gaps have long-term structural consequences. Delayed action can entrench fossil-fuel-dependent infrastructure, creating technological “lock-ins” that make future decarbonisation more difficult and expensive. Emerging economies risk falling behind in the adoption of breakthrough low-carbon technologies, which could widen the global technology gap and limit competitiveness in energy-intensive industries.

“Delayed action can entrench fossil-fuel-dependent infrastructure, creating technological ‘lock-ins’ that make future decarbonisation more difficult and expensive.”

Policy gaps also have social and equity implications. Workers and communities reliant on high-emission industries may face economic disruption if transitions are unplanned or delayed, while inadequate energy infrastructure can constrain access to affordable, clean energy for households and smaller enterprises. In this sense, industrial decarbonisation is not solely an environmental imperative; it is a crucial element of sustainable, inclusive economic development.

Taken together, these dynamics illustrate that policy deficiencies undermine not only climate targets but also broader economic modernisation, industrial competitiveness, and societal resilience. In emerging economies, closing these gaps is essential to turn net-zero ambitions into tangible outcomes, making it clear why international actors, technical partnerships, and blended finance mechanisms are critical in supporting governments and industry to implement actionable solutions. Bridging these implementation gaps, however, is rarely achievable by domestic governments alone; emerging economies often require the support of international actors who can provide technical expertise, mobilise finance, and facilitate multi-stakeholder coordination, translating policy ambition into actionable industrial decarbonisation strategies.

“Policy deficiencies undermine not only climate targets but also broader economic modernisation, industrial competitiveness, and societal resilience.”

Industrial decarbonisation in emerging economies is tough — the challenges are technical, financial, and political all at once. This is where international actors step in, not just as advisers, but as connectors. They bring governments, businesses, and investors together, helping turn net-zero ambitions from plans on paper into real-world results.

From providing technical guidance and sector-specific roadmaps to mobilising blended finance and setting global standards, these organisations act as the glue that links policy, innovation, and investment. Without this kind of support, high-emission sectors like steel, cement, and chemicals would struggle to transition at the pace and scale required to meet climate goals — especially in the Global South, where structural and financial barriers are toughest.

“International actors act as the glue that links policy, innovation, and investment, helping turn net-zero ambitions from plans on paper into real-world results.”

UNIDO provides technical assistance to design sector-specific decarbonisation pathways, strengthen MRV systems, and build institutional capacity. For example, its Industrial Energy Efficiency Programme assists governments and enterprises in conducting energy audits, establishing efficiency standards, and creating incentive mechanisms. Through the Net Zero Partnership for Industrial Decarbonization, UNIDO offers in-country support for the deployment of breakthrough technologies, electrification of heat, and process emissions reduction, while also facilitating access to blended finance to make projects bankable. These interventions exemplify how international actors act as intermediaries, connecting governments, private industry, and financiers to overcome barriers in implementation.

The IEA supports emerging economies with globally recognised sectoral roadmaps for industrial decarbonisation. Its Net Zero by 2050 Roadmap provides detailed pathways for heavy industries, modelling technology options, investment needs, and emissions outcomes. By offering quantitative guidance and scenario analysis, the IEA helps countries prioritise interventions and allocate resources efficiently, reducing the risk of stranded assets and ineffective policy measures.

The World Bank Group and IFC provide concessional finance, risk mitigation instruments, and advisory services. A notable example is the Climate Investment Funds’ Industry Decarbonization Investment Programme, which mobilises blended finance to scale industrial decarbonisation projects across emerging markets. These programmes not only provide capital but also act as conveners, aligning public and private stakeholders to co-invest in high-emission sectors, such as cement plants and steel mills in India, Indonesia, and Brazil.

Funds such as the Green Climate Fund (GCF) and the Global Environment Facility (GEF) support early-stage project preparation, grants, and concessional loans. For example, GCF funding has been deployed to pilot carbon capture and storage (CCS) in cement manufacturing and to incentivise energy-efficient process retrofits in chemical plants, providing proof-of-concept models that can be scaled by the private sector.

Regional banks, including the African Development Bank (AfDB), Asian Development Bank (ADB), and Inter-American Development Bank (IDB), offer both financing and policy support tailored to regional industrial structures. Their programmes include low-carbon industrial parks, energy-efficient infrastructure, and renewable energy integration into industrial zones. By coordinating with national governments, these banks help ensure that industrial decarbonisation aligns with regional development goals and infrastructure planning.

Global initiatives such as the Mission Possible Partnership, the Energy Transitions Commission (ETC), and GFANZ convene private and public stakeholders, providing frameworks for decarbonising hard-to-abate sectors. For instance, the Mission Possible Partnership has developed sectoral pathways for steel and chemicals, enabling investors to commit capital with confidence and governments to embed clear targets into policy. These partnerships demonstrate how collaborative knowledge platforms act as intermediaries, bridging gaps between innovation, finance, and regulatory frameworks.

Technical bodies such as ISO and the Global Green Growth Institute (GGGI) support harmonised MRV protocols and industry standards, enabling transparent, comparable, and credible measurement of emissions. Such standards are essential for verifying industrial decarbonisation outcomes, integrating emissions data into carbon pricing, and attracting private investment.

In summary, these international actors and programmes collectively serve as middlemen between governments, industry, and finance, facilitating innovation, aligning incentives, and providing the technical, financial, and policy infrastructure necessary to make industrial decarbonisation achievable. Their interventions are particularly crucial in the Global South and emerging economies, where structural and financial barriers often limit the translation of net-zero ambitions into concrete action. By combining public mandates, private investment, and technical expertise, these actors help ensure that industrial decarbonisation is both feasible and scalable.

Even with ambitious net-zero targets, emerging economies face persistent gaps in turning plans into action. Limited technical capacity, constrained financing, fragmented governance, and weak regulatory frameworks all slow progress. Beyond these immediate obstacles, research shows that even well-intentioned climate policies can produce unintended consequences, or “problem-shifts,” affecting other sectors, regions, and future generations (Adipudi, Kim & Biermann, 2025).

“Even well-intentioned climate policies can produce unintended consequences, or ‘problem-shifts,’ affecting other sectors, regions, and future generations.” (Adipudi, Kim & Biermann, 2025)

For instance, the study highlights several concrete cases:

- Energy-efficient technologies: Promotion of compact fluorescent lamps (CFLs) in high-income countries reduced emissions locally, but the disposal of used CFLs exported hazardous waste — mercury and lead — to informal recycling sites in Ghana and Nigeria. This caused serious neurodevelopmental harm and environmental contamination, illustrating how a policy that mitigates emissions in one region can generate environmental and social burdens elsewhere.

- Biofuel policies: EU mandates initially incentivised converting biodiverse or high-carbon landscapes into biofuel crops. While emissions decreased in Europe, these policies indirectly drove land-use change and ecosystem loss in parts of Africa and South America, showing the cross-regional ripple effects of industrial and energy policies.

- Carbon capture and storage (CCS): CCS deployment in some industrialized contexts lowered direct CO₂ emissions but prolonged fossil fuel use, increased water demand, and placed additional pressures on land for bioenergy crops. This underscores the importance of evaluating systemic and resource-related impacts alongside emissions reductions.

- Renewable energy projects: Large-scale wind, solar, and hydropower developments sometimes disrupted local ecosystems or water flows, while poorly planned afforestation efforts introduced alien species or strained water resources, highlighting the need for integrated environmental assessments.

- Emissions trading schemes: Carbon markets successfully lowered emissions locally in the Global North but, in some cases, unintentionally shifted pollution, economic burdens, or food insecurity to the Global South through carbon leakage or changes in trade and land-use patterns.

“Gaps between promised and implemented climate actions can slow progress and shift impacts across sectors and regions.” (Adipudi, Kim & Biermann, 2025)

These examples illustrate a critical lesson: industrial decarbonisation is not just a technical or financial challenge. Policies designed to reduce emissions in one area may shift burdens across sectors, regions, or generations, particularly affecting emerging economies that are less able to absorb these impacts.

Without careful design, interventions aimed at reducing emissions in one area can shift burdens elsewhere or into the future.

At the same time, industrial emissions are inherently hard to eliminate. Even if electricity grids are fully decarbonised and transport electrified, sectors like steel, cement, chemicals, and heavy machinery remain substantial sources of emissions (Ritchie, 2020). This is due to:

- High-temperature energy demand: Industrial processes require temperatures only achievable with fossil fuels or currently costly alternatives, such as hydrogen, bioenergy, or concentrated solar heat.

- Process emissions: Some CO₂ emissions are a chemical byproduct of production, as in cement or chemical manufacturing. These cannot be addressed by switching to low-carbon electricity alone.

- Global supply chain effects: Industrial outputs feed into construction, transport, and consumer goods, producing indirect “embedded” emissions worldwide.

Given this context, translating ambition into practical action demands a multi-layered approach, combining policy, finance, technical support, and cross-sectoral awareness. Emerging economies, in particular, must carefully balance decarbonisation with economic growth, employment, and industrial competitiveness.

Emerging economies often set ambitious industrial decarbonisation targets, but policy gaps can slow progress. The actions provided below offer practical steps to turn ambition into real-world implementation.

By combining these measures, emerging economies can tackle industrial emissions strategically, seizing opportunities for innovation, job creation, and cleaner production. The path to industrial decarbonisation is not just about reducing CO₂ — it’s about modernising industry, aligning economic and climate priorities, and embedding equity into policy design.

Even with ambitious net-zero targets, emerging economies still face persistent implementation gaps in industrial decarbonization. Challenges such as limited technical capacity, inadequate financing, and weak regulatory frameworks often prevent policy commitments from translating into real emission reductions.

This is where actors like UNIDO and its Net Zero Partnership for Industrial Decarbonization play a crucial role. Through this initiative, UNIDO provides tailored in-country support, helping governments and industries implement practical solutions in high-emission sectors such as cement, steel, and energy-intensive manufacturing. Their approach is multi-faceted:

- Technology deployment: Supporting energy efficiency upgrades, electrification of heat where feasible, and the adoption of breakthrough low-carbon technologies.

- Process innovation: Guiding industries in reducing process emissions, such as carbon released from cement production or chemical manufacturing.

- Financing and investment: Mobilizing public and private capital, providing blended finance mechanisms, and creating bankable projects to overcome financial barriers.

- Policy integration: Assisting governments in designing regulations, standards, and incentives that enable industrial decarbonization to scale effectively.

By linking these interventions to real-world industrial operations, UNIDO bridges the gap between ambition and implementation, demonstrating that policy targets can be transformed into measurable emission reductions. In emerging economies, where industrial emissions are both growing and hard to abate, such coordinated support is indispensable — without these actors, net-zero goals risk remaining aspirational rather than actionable.

Industrial decarbonisation in emerging economies remains a complex challenge, where the imperatives of economic growth, energy-intensive production, and climate commitments intersect. Policy gaps — in sector-specific planning, incentives, financing, and measurement, reporting and verification (MRV) systems — often prevent ambitious targets from being translated into concrete emission reductions.

International actors and programmes, such as UNIDO’s Net Zero Partnership for Industrial Decarbonization, the World Bank’s Industry Decarbonization Investment Programme, the Climate Investment Funds, and regional development banks, play a pivotal role as intermediaries. They help governments design actionable policies, mobilise blended finance, facilitate technology deployment, and integrate innovative solutions into industrial operations. These initiatives exemplify public–private collaboration, connecting domestic industries with global expertise, capital, and technical support to overcome the structural and financial barriers common in the Global South.

By bridging ambition and implementation, these coordinated efforts enable emerging economies to tackle high-emission sectors such as cement, steel, and chemicals, modernise industrial infrastructure, and turn net-zero goals into measurable, scalable outcomes. Addressing these challenges effectively requires a multi-stakeholder approach in which policy, innovation, and finance converge, ensuring that industrial growth is both climate-compatible and economically resilient.